One of the first questions most property buyers ask is:

“How much mortgage can I actually get?”

In Abu Dhabi, the answer depends on several factors, including your income, current financial obligations, and individual bank policies. Understanding your mortgage eligibility early can help you focus on properties within your budget and avoid unnecessary delays during the buying process.

What Determines Your Mortgage Eligibility in Abu Dhabi?

Banks in the UAE evaluate your borrowing capacity using three key factors:

• Income level

• Existing liabilities

• Credit profile

However, the most important factor is your Debt Burden Ratio (DBR).

What is DBR (Debt Burden Ratio)?

DBR refers to the percentage of your monthly income that can be allocated toward loan repayments.

In the UAE:

Maximum DBR is typically 50%

This means:

• All monthly financial commitments (personal loans, credit cards, and mortgage payments)

• Should not exceed 50% of your monthly income

Real Examples (Based on UAE Market)

Example 1: AED 15,000 Salary

• Maximum total commitments: ~AED 7,500

• Estimated mortgage eligibility: AED 800K – 1M

Example 2: AED 25,000 Salary

• Maximum commitments: ~AED 12,500

• Estimated mortgage eligibility: AED 1.5M – 2M

Example 3: AED 40,000 Salary

• Maximum commitments: ~AED 20,000

• Estimated mortgage eligibility: AED 2.5M – 3.5MThese are estimated ranges only. Final approval depends on:

• Interest rate

• Loan tenure

• Existing liabilities

• Bank policy

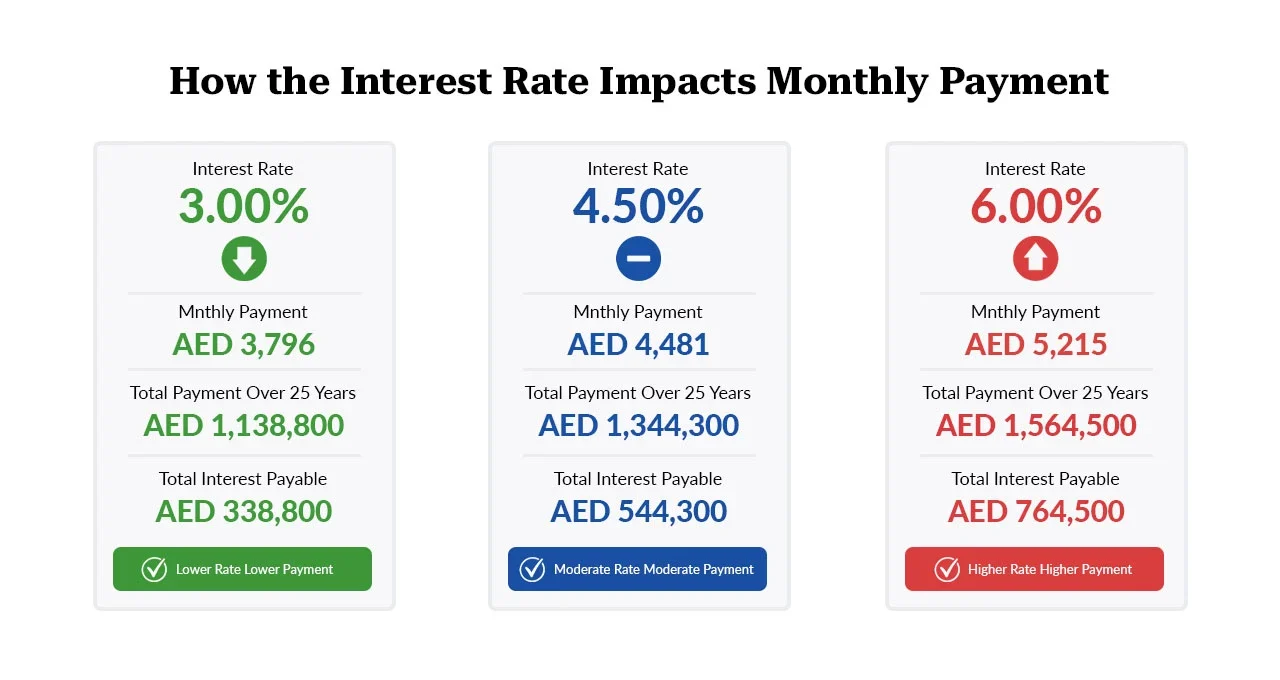

How Interest Rates Affect Your Mortgage Amount

Mortgage eligibility is not fixed, it changes depending on interest rates and bank affordability calculations.

In the UAE, many mortgages are linked to EIBOR (Emirates Interbank Offered Rate).

If interest rates increase:

• Your monthly instalment increases

• Your borrowing capacity decreases

If interest rates decrease:

• Your monthly instalment becomes lower

• Your mortgage eligibility may improve

To learn more about how EIBOR affects mortgage pricing, read this article: How EIBOR Drives Mortgage Pricing: Understanding Low-Interest Mortgage in Abu Dhabi

Real Impact Example

AED 2M mortgage:

• 0.25% rate drop → ~AED 5,000 savings per year

• 0.50% drop → AED 10,000+ savings per year

This is why mortgage timing and rate structure play an important role in your overall affordability.

Loan Tenure and Its Impact

The longer your mortgage tenure:

• The lower your monthly instalment

• The higher your potential loan amount

Typical mortgage tenure in the UAE:

Up to 25 years

However, banks also take the following into consideration:

• Maximum age at loan maturity

• Retirement planning

Minimum Down Payment in Abu Dhabi

According to UAE Central Bank regulations:

• UAE Nationals → from 15%

• Expat Residents → from 20%

• Non-Residents → from 40%+

Properties priced above AED 5M usually require a higher down payment.

Other Factors That Affect Your Approval

In addition to income, banks also assess:

• Credit score (AECB)

• Employment stability

• Industry risk

• Existing loans and credit cards

• Property type

Common Mistakes Buyers Make

• Overestimating how much they can borrow

• Ignoring existing liabilities

• Failing to account for interest rate changes

• Searching for a property before getting pre-approval

• Assuming all banks offer the same mortgage terms

Why Mortgage Pre-Approval Matters?

Many buyers attempt to estimate their budget on their own.

The smarter approach is:

Get pre-approved first

This gives you:

• A more accurate loan amount

• Clear affordability expectations

• Stronger confidence when negotiating with sellers

How Prime Rate Hub Helps You Maximise Your Eligibility

At Prime Rate Hub, we do more than calculate your mortgage eligibility. We help optimise it.

We help you:

• Compare mortgage options across 20+ UAE banks

• Structure your application correctly

• Minimise the impact of existing liabilities

• Match with banks offering higher approval potential

• Secure competitive rates and flexible terms

This ensures you don’t just get approved, but also get the most suitable mortgage solution for your situation.

Conclusion

Your mortgage eligibility in Abu Dhabi depends on much more than just your salary.

It is influenced by:

• Income

• Financial commitments

• Interest rates

• Bank policy

Understanding these factors early allows you to make informed financial decisions, plan your property search effectively, and avoid delays during the mortgage process.

Frequently Asked Questions

Mortgage eligibility is calculated based on your income, liabilities, and DBR, which is generally capped at 50%.

Yes. You may improve your eligibility by reducing liabilities, extending the loan tenure, or applying through the right bank.

No. Banks also consider your credit score, employment stability, and existing liabilities.

Yes, provided your total financial commitments remain within the DBR limit.

Mortgage tenure in the UAE is typically up to 25 years, depending on your age and the bank’s policy.

Yes, although financing limits are lower and eligibility requirements are generally stricter.

Yes. Higher EIBOR rates can reduce affordability and lower your borrowing capacity.

Yes. Mortgage pre-approval helps ensure you search within your actual and approved budget.

About Prime Rate Hub

Prime Rate Hub is a mortgage brokerage based in Abu Dhabi, partnering with more than 20 UAE banks to support clients with mortgage pre-approval, property financing, refinancing, and mortgage buyout solutions.