Introduction

Most property buyers in Abu Dhabi begin by searching for the right property. In reality, the more effective first step is understanding how much you can borrow.

Mortgage pre-approval provides clarity before you enter the market. It defines your budget, strengthens your position as a buyer, and enables you to move quickly when the right opportunity arises.

What is Mortgage Pre-Approval?

Mortgage pre-approval is an initial assessment by a bank confirming that you meet the eligibility criteria for a home loan.

The bank evaluates your:

• Income

• Existing liabilities

• Credit profile

• Employment stability

Based on this assessment, the bank issues a pre-approval letter indicating the loan amount you may qualify for.

This approval is typically valid for 30 to 90 days and allows you to begin your property search with confidence.

Why Pre-Approval is Important in Abu Dhabi

Many buyers underestimate the importance of pre-approval.

In practice, it provides:

• Clear budget visibility before searching

• A stronger position when negotiating with sellers

• A faster transaction process

• Reduced risk of rejection at a later stage

Without pre-approval, buyers often spend time viewing properties outside their eligibility range.

How Much Mortgage Can You Get in Abu Dhabi?

Your eligibility is primarily based on the Debt Burden Ratio (DBR).

In the UAE, banks typically cap DBR at 50% of your monthly income. This means your total loan commitments should not exceed half of your income.

Example (Indicative Only)

• AED 15,000 salary → approx. AED 1M – 1.3M loan

• AED 25,000 salary → approx. AED 1.5M – 2.2M loan

• AED 40,000 salary → approx. AED 2.5M – 3.5M loan

Actual approval depends on your liabilities, credit score, and the bank’s internal policy.

Banks may also apply a stress test by increasing interest rates by 1–3% to ensure affordability under higher rate conditions.

Minimum Down Payment Requirements

Based on UAE Central Bank regulations:

• UAE Nationals → from 15%

• Expat Residents → from 20%

• Properties above AED 5M → higher down payment required

Down payments must come from your own funds and cannot be financed through personal loans.

Documents Required for Pre-Approval

For salaried applicants:

• Passport and Emirates ID

• Salary certificate

• Last 3–6 months bank statements

• Credit report (AECB)

• Details of existing liabilities

For self-employed:• Trade license

• Financial statements (usually 2 years)

• Company documents

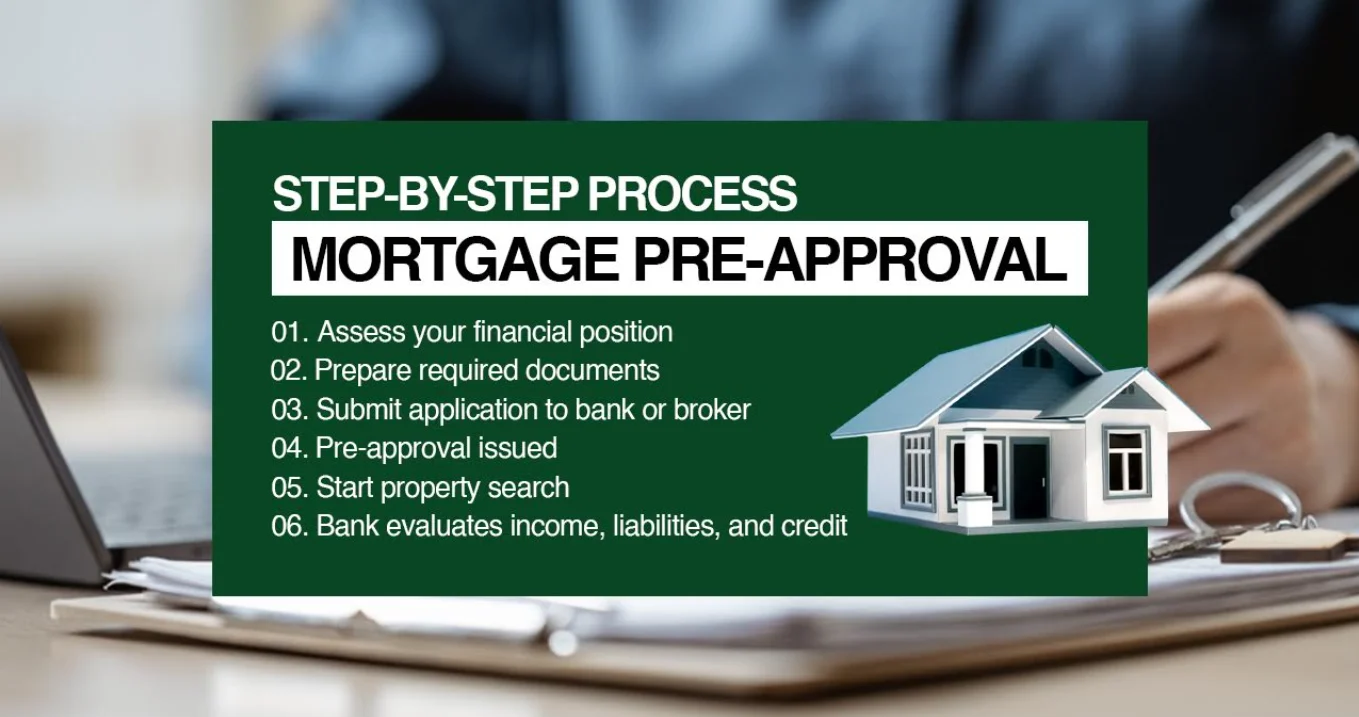

Step-by-Step Mortgage Pre-Approval Process

- Assess your financial position

- Prepare required documents

- Submit application to bank or broker

- Bank evaluates income, liabilities, and credit

- Pre-approval issued

- Start property search

The process usually takes 3–7 working days if documents are complete.

Common Mistakes to Avoid

• Searching for property before pre-approval

• Ignoring existing liabilities

• Applying with the wrong bank

• Not comparing multiple lenders

• Assuming pre-approval guarantees final approval

Pre-approval confirms eligibility, but final approval depends on the property and updated checks.

The Role of Prime Rate Hub

Mortgage pre-approval is not just about getting approved. It is about getting approved correctly.

At Prime Rate Hub, our role includes:

• Comparing options across 20+ UAE banks

• Matching your profile with the most suitable lender

• Structuring your application to meet bank requirements

• Speeding up approval timelines

• Reducing the risk of rejection

This ensures your pre-approval aligns with your actual property plans.

When Should You Apply for Pre-Approval?

The timing is straightforward:

Before you start viewing properties

This allows you to:

• Focus only on properties within your budget

• Avoid unnecessary delays

• Act quickly when you find the right unit

Frequently Asked Questions

Usually between 2 to 4 working days, depending on the bank and documentation.

It is not legally required, but it is strongly recommended before starting your property search.

No. Final approval depends on property valuation and updated financial checks.

Typically between 30 to 90 days.

Yes, but working with a broker is more efficient as they can compare options without unnecessarily impacting your profile.

It may involve a credit check, which is standard as part of the process.

You will need to reapply with updated documents.

Yes, but with stricter criteria and lower financing limits.

Conclusion

Mortgage pre-approval is one of the most important steps in the home buying process in Abu Dhabi.

It provides financial clarity, improves decision-making, and ensures you enter the market as a prepared and serious buyer.

About Prime Rate Hub

Prime Rate Hub is a mortgage brokerage based in Abu Dhabi, working with over 20 UAE banks to support clients with pre-approval, property financing, refinancing, and buyout solutions.