For many property buyers in Abu Dhabi, choosing the right property is often easier than understanding the mortgage process itself.

From mortgage pre-approval to final property transfer, the journey involves several stages, banks, developers, valuation companies, and transfer authorities. Without proper guidance, the process can quickly become confusing and time-consuming.

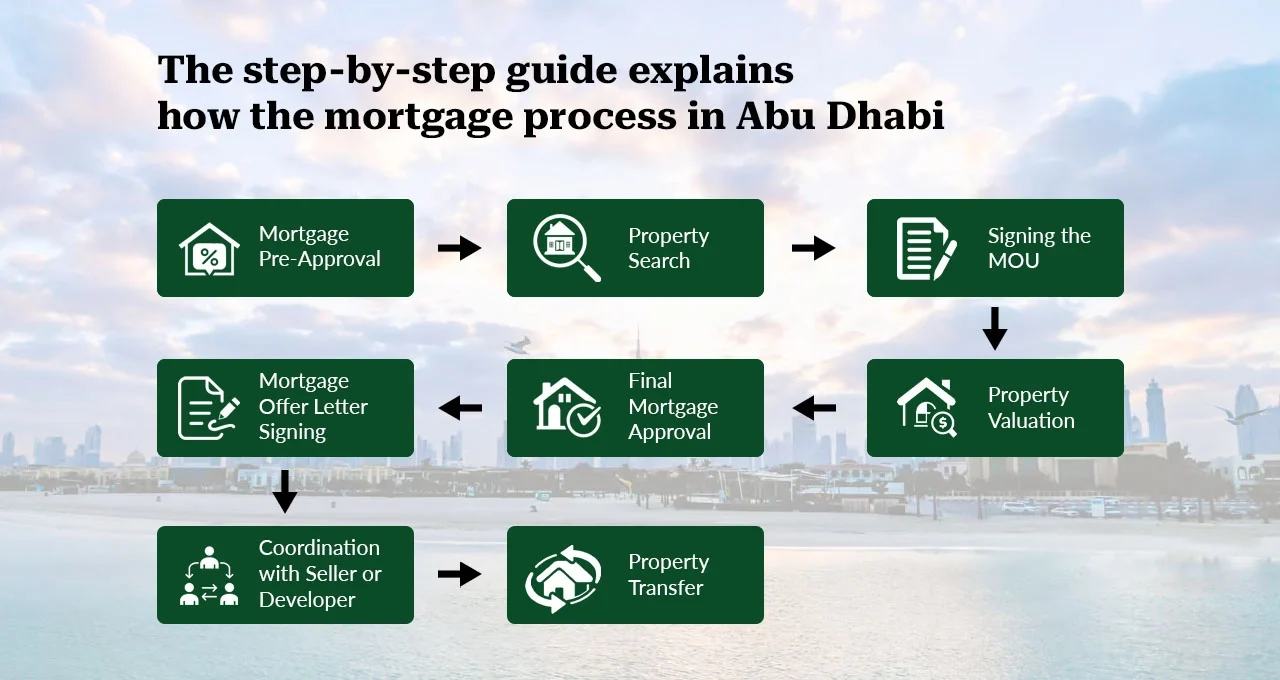

This step-by-step guide explains how the mortgage process in Abu Dhabi works in 2026, including timelines, approvals, property valuation, and the final transfer stage, so you know exactly what to expect before starting your home-buying journey.

Step 1: Mortgage Pre-Approval

The first stage in the mortgage process is obtaining mortgage pre-approval from the bank.

At this point, the bank reviews your:

- Monthly income

- Existing financial liabilities

- Credit profile and repayment history

Based on this assessment, the bank issues a pre-approval letter confirming the amount you are eligible to borrow.

This helps buyers understand their actual purchasing power before searching for a property.

Typical timeline: 2–5 working days

Step 2: Property Search

Once your mortgage pre-approval is secured, you can begin searching for a property that fits within your approved budget.

This step is important because it helps:

- Narrow down eligible properties

- Prevent financing complications later

- Speed up the approval process

Buyers usually explore either resale properties or developer projects depending on their investment goals and financing preferences.

Step 3: Signing the MOU (Memorandum of Understanding)

After selecting a property, the buyer and seller move forward with signing the Memorandum of Understanding (MOU).

At this stage:

- The sale price is agreed upon

- Terms and conditions are confirmed

- A deposit cheque (usually 10%) is submitted

The MOU officially formalises the agreement between both parties before the bank proceeds with the next mortgage stages.

Step 4: Property Valuation

The bank then appoints an authorised valuation company to assess the property’s market value.

The valuation is conducted to:

- Verify the actual market value of the property

- Ensure the requested loan amount is justified

- Reduce lending risk for the bank

If the valuation amount comes lower than the agreed purchase price, the buyer may need to increase the down payment.

Typical timeline: 2–4 working days

Step 5: Final Mortgage Approval

Once the valuation report is completed and approved, the bank issues the final mortgage approval.

At this stage:

- Loan terms are confirmed

- The applicable interest rate is finalised

- The mortgage offer letter is prepared

- Bank account opening may be completed if required

This is one of the most important stages because the financing structure becomes officially confirmed.

Typical timeline: 3–5 working days

Step 6: Mortgage Offer Letter Signing

The buyer then signs the official mortgage offer letter issued by the bank.

This document includes:

- Approved loan amount

- Interest rate details

- Repayment structure

- Mortgage tenure and conditions

Signing the offer letter confirms acceptance of the mortgage terms and allows the process to move toward transfer coordination.

Step 7: Coordination with Seller or Developer

This stage involves coordination between multiple parties, depending on whether the property is resale or developer-owned.

For Resale Properties

- Existing seller liabilities are settled (if applicable)

- Bank prepares the payment structure

- Transfer arrangements are coordinated

For Developer Properties

- Final payment schedules are arranged

- Developer documentation and NOC procedures are completed

The process may involve coordination with:

- The bank

- Seller or developer

- Abu Dhabi Municipality (ADM)

- Abu Dhabi Global Market (ADGM)

- Trustee offices

Step 8: Property Transfer

The final step is the official property transfer.

This usually takes place at:

Abu Dhabi Municipality / Trustee Office / Abu Dhabi Global Market (for Al Reem Island properties)

At this stage:

- The bank releases the mortgage funds

- Ownership is officially transferred

- The title deed is issued to the buyer

Once completed, the mortgage process is considered finalised.

Typical Mortgage Timeline in Abu Dhabi

In most cases, the complete mortgage process takes approximately:

4 to 7 weeks

However, timelines may vary depending on:

- Document readiness

- Bank processing speed

- Property type

- Developer approvals

- Seller mortgage clearance requirements

Common Reasons for Mortgage Delays

Several factors can slow down the mortgage approval and transfer process, including:

- Missing or incomplete documentation

- Lower-than-expected property valuation

- Existing seller mortgage liabilities

- Bank policy mismatches

- Delays in obtaining developer NOC approvals

Understanding these risks early can help buyers avoid unnecessary complications and delays.

How EIBOR Affects Your Mortgage After Approval

Many buyers focus only on mortgage approval without considering how rates may change after the transfer stage.

Most UAE mortgages eventually move to:

This means your monthly instalment can increase or decrease depending on market conditions.

Example:

For an AED 2 million mortgage:

- A 0.25% rate reduction could save approximately AED 10,000 annually

- A 0.50% reduction could result in savings exceeding AED 20,000 per year

Understanding EIBOR is important for long-term financial planning.

The Role of Prime Rate Hub

The mortgage process involves continuous coordination between banks, valuation companies, developers, sellers, and transfer authorities.

At Prime Rate Hub, the process is managed end-to-end through:

- Mortgage pre-approval assistance

- Bank matching and comparison

- Documentation preparation

- Valuation coordination

- Final approval management

- Property transfer support

This helps clients benefit from:

- Faster processing timelines

- Reduced delays

- Better mortgage structuring

- Smoother communication between all parties

Conclusion

The mortgage process in Abu Dhabi follows a structured system, but successful completion depends heavily on planning, documentation, and proper coordination.

Understanding each stage from pre-approval to property transfer allows buyers to navigate the process more confidently while reducing the risk of unnecessary delays or financing issues.

Frequently Asked Questions

The process usually takes around 4–7 weeks depending on the bank, property type, and documentation readiness.

Mortgage pre-approval is the first and most important step.

Yes, but it may increase the risk of financing delays or rejection later in the process.

You may need to increase your down payment to cover the difference.

Funds are usually released during the final property transfer stage.

Yes. Delays can occur due to documentation issues, valuation concerns, developer approvals, or bank processing timelines.

The overall structure is similar, but approval timelines and policies vary between banks.

Yes. The coordination process and payment structures can differ depending on the property type.

About Prime Rate Hub

Prime Rate Hub is a mortgage brokerage based in Abu Dhabi, working with more than 20 UAE banks to assist clients with mortgage pre-approvals, home financing, refinancing, and property transfer support.